If you have come from a country where you have credit bureaus, you know how important your credit history can be. Your credit history can dictate:

- the interest rate you will pay on your mortgage

- your ability to be approved for lines of credit, and

- your eligibility for employment in some finance related roles.

So what is your credit score when you come to Canada? Nothing. Think of it as a blank slate. Everything you do henceforth will dictate if your credit score goes up or down. Even the simple act of going down is cause for concern and can be seen by all lenders so listen up.

Canadian lenders typically check each applicant’s credit files at one of the main credit reporting agencies (Equifax Canada and TransUnion). This file is like a financial report card that tracks how much you borrow and how quickly you pay it back, to calculate your credit rating and credit score.

Without a credit history, newcomers may be told they need a loan co-signer with a Canadian credit rating, considerable assets as collateral, or they must demonstrate a history of stable income in Canada to receive a loan.

Fortunately, you can establish a Canadian credit history and start building a credit record shortly after you arrive in Canada.

Recommended Posts:

Top 10 financial steps to take before you leave for Canada

First things to do after landing in Canada

Tips to Maintain a Good Credit Report in Canada

Renting Without a Credit History

Banking and Finance in Canada: Your First Steps

Your credit history or credit rating starts the first time you get a credit card or loan in your name from a Canadian bank. You can begin by applying for and using a credit card responsibly.

Even if you don’t have immediate plans to buy a house or vehicle, it’s a good idea to establish a credit history, since banks may give special consideration to recent newcomers.

In some cases, newcomers may be offered a ‘secured’ credit card. A secured credit card is different than a regular credit card because it requires a security deposit equal to the amount of the credit limit. Think of it as a stepping stone to getting an unsecured credit card. Such special offers may be more difficult to obtain later, especially if your income does not grow as fast as you had hoped. A credit card is also useful for larger purchases and as a secondary piece of identification.

Why your credit history is important

Your credit score is important for a number of reasons:

- Lenders will review your credit score, for example when you want a mortgage to buy a home, or a loan to buy a car. They want to understand your history and ability to manage credit and pay off debt.

2. Most landlords will conduct a credit check before they rent their property to you.

3. Some employers will conduct a credit check before they make an offer of employment. This is common with banks and other financial institutions such as insurance companies.

Understanding your credit history score

Once you receive a credit card, use it wisely to establish a credit score so that lenders will have confidence in your ability to re-pay loans.

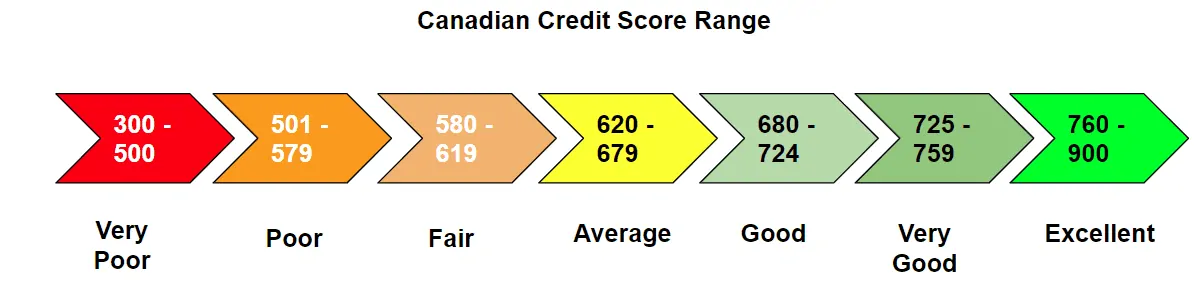

Your credit is scored on a point system that ranges from 300 – 900 points, where 900 is the best score. To qualify for a standard loan, it’s best if you score 650 points or higher. If you score lower than 650, it will be difficult to get a loan or receive new credit. However, if you have a low credit score, you can improve your score by carefully managing your credit use.

Use credit carefully

Once you receive credit, use it wisely to build a good credit history:

Do use your new credit card to create a credit history. Make purchases with the card, but pay your bills in full and on time.

Be aware of the interest rate charges if you do not pay the balance in full each month.

Don’t go over the credit card limit.

If you can’t pay the full balance on your credit card, at least pay the minimum balance and make regular payments, with the goal of paying off debts as quickly as possible.

Don’t apply for credit too often since too many credit cards can hurt your credit rating.

Try not to use more than 30% of your credit limit (also known as a balance-to-limit ratio).

Avoid opening many credit accounts. Many credit card accounts can signal financial distress to lenders, especially is they all carry a balance on them.

Live within your financial means. As the saying goes, “It’s not how much you earn, it’s how much you spend.”

When you manage how you use credit, you’ll remain in good financial standing and be able to secure credit to achieve your important dreams.